Holidays Recap and Review

Quick year review on Gold

First and foremost, hope all of you have had a great holidays and had the chance to spend with family and friends and get the bes of 2024. This season is also very good to review the year and set your next targets with eyes on long term objectives. Hope you also had the chance to review your strengths and weaknesses and now it’s time to transform those weaknesses into strengths and fine tune the best of yourself for greater achievements.

During our absence, we notice that Gold and Dollar kept the sentiment reinforced by Jerome Powell on FOMC decision day with the rate cuts narrative holding the most weight during the entire Christmas and new years season.

At the start of December we had Gold hitting new ATH at 2146 with algos adjusting to “unsailed sea” prices and then after optimistic labor data as we covered, focus was on CPI and FOMC SEP projections.

With CPI within expectations and forecast, FOMC day on 13th with dovish SEP and Jerome Powell speech set the tone to what was to come. The rate cut narrative got its strength not only making Gold to keep trading above the 2000s psychological price point creating that bullish trend channel at previous chart but also closed of the year and month at 2062 mark price.

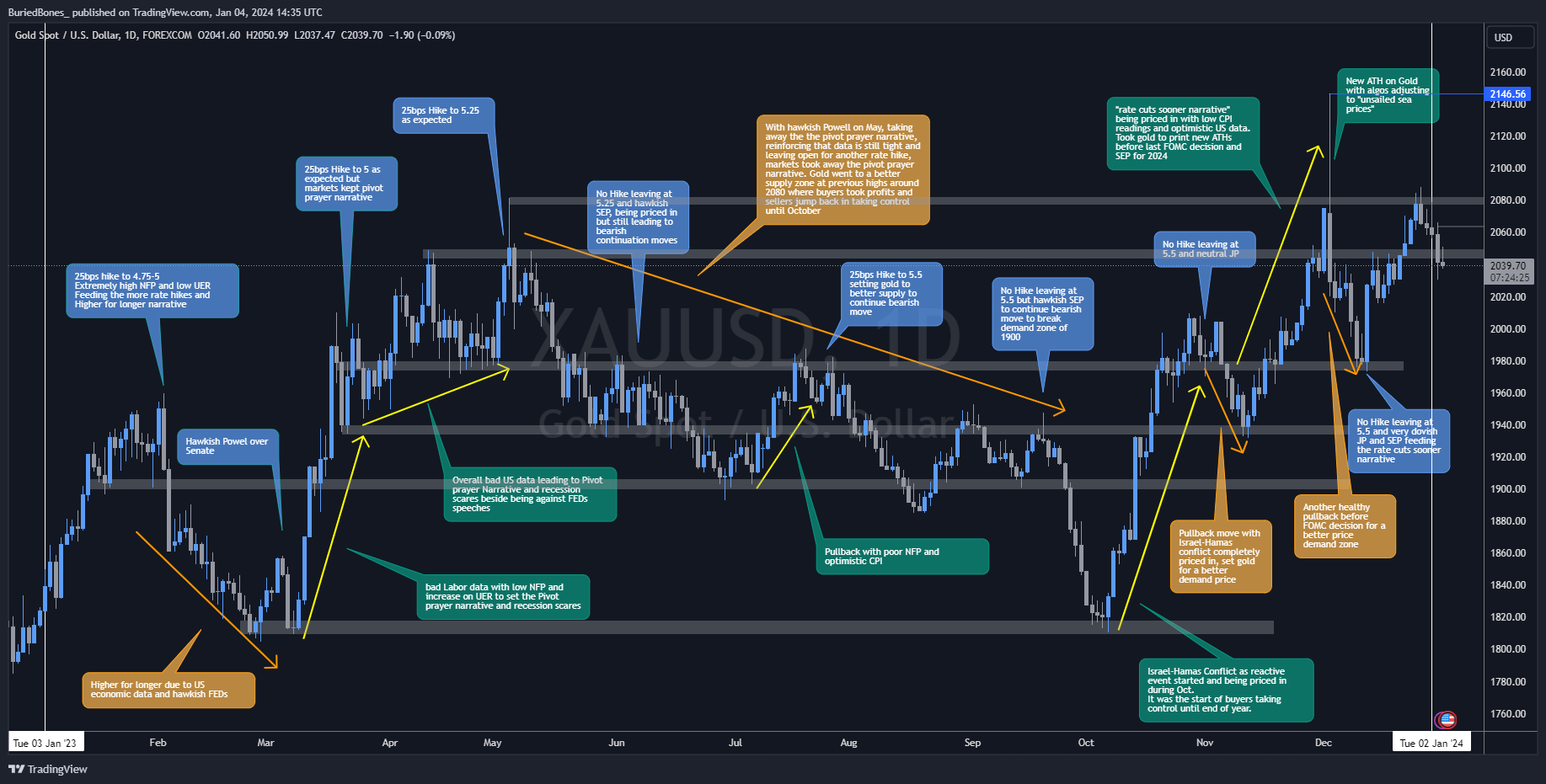

Looking now on a macro level, and doing an overview on Gold, the year was pretty interesting as we have some narrative shifts that set the sentiment and Gold direction.

If you can not see the image properly, you can go directly on Tradingview. As we can see, we start the year with the rates higher for longer narrative, as hawkish FEDs hold some weight on the first quarter and with recessionary scares US data we started to play the “Pivot Prayer” narrative that hold until May. On FOMC day of May, Hawkish Powell leaving the door open for more rate hikes killed the pivot prayers narrative and brought back the “rates higher for longer” where sellers jump back in from a better supply area on the previous highs of 2080 and took control of Gold movement until the start of Israel-Hamas conflict. We can see a downside move from the 2080 where the September SEP made gold to break the 1900 straight down to 1800.

Interesting fact that Gold went to a major demand area where the reactive event of Israel-Hamas conflict shifted the sentiment for the entire month of October, where buyers provided the exit relief of sellers leading gold to hit the 2000 mark without any pullbacks as we were very vigilant for reactive headlines that could push Gold to the upside. With November arriving and with a neutral Jerome Powell, we saw the first healthy pullback from the reactive headlines, telling us that the conflict was already priced in and a new narrative came into play as we were approaching the end of the year and important holidays break with Thanks Giving, Christmas and New Year was right on the corner. With the pullback to a better demand at 1930, Gold start is last upside move of the year supported by low CPI readings and optimistic US data, making economist and investors pricing in “Sooner rate cuts” as all the expectations were to occur only on the 2nd half of 2024 and we close of the year with cut expectations to occur in March. Such made Gold to print new ATHs at 2146, where we saw algos adjusting to “unsailed sea prices” and such narrative made not only gold failed to break lower than 2000 but closing the year at 2060.

Very quick and short summary on Gold for the year and now what?

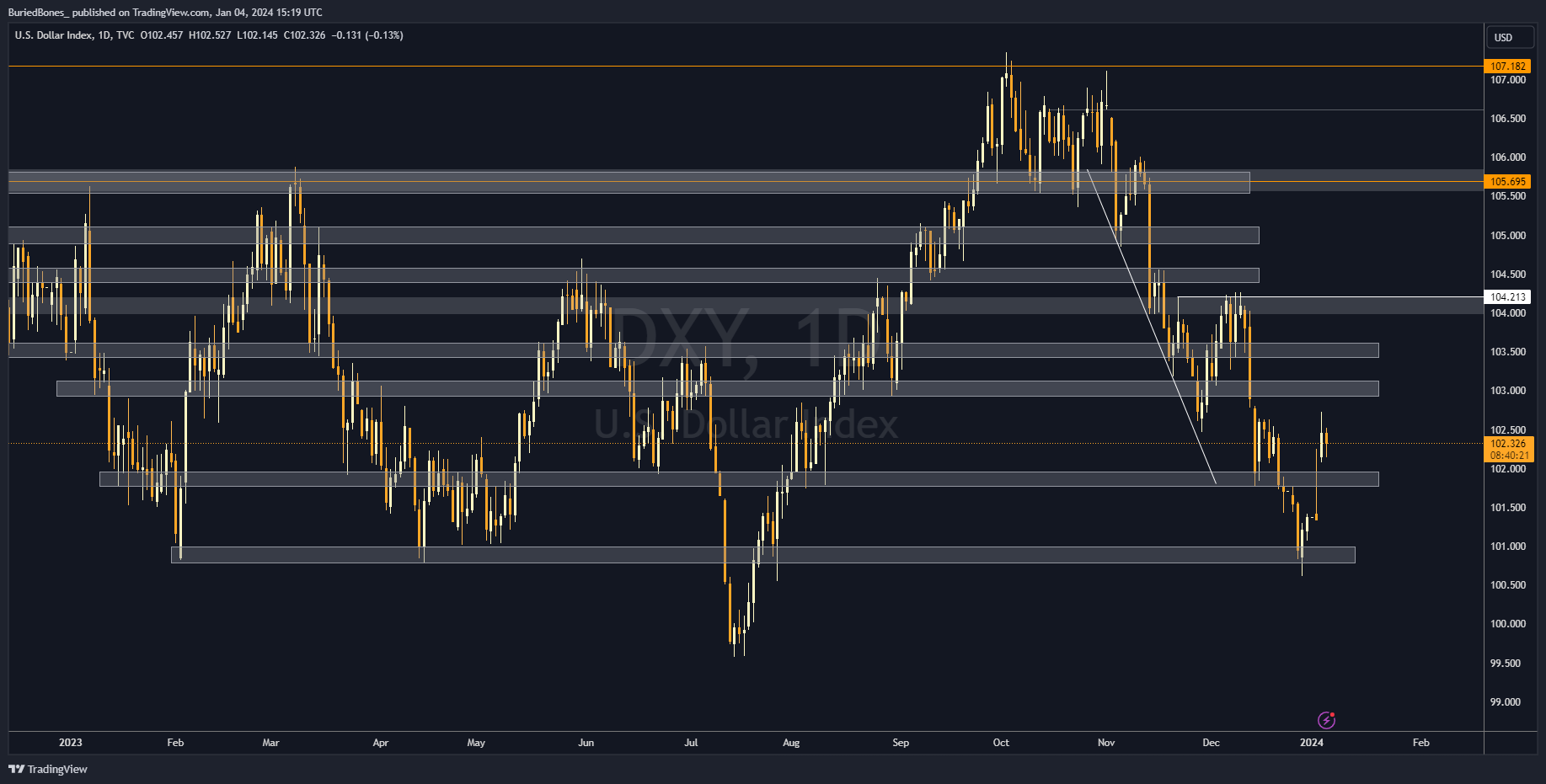

This week, smaller than usual due to new year, our expectations were to be slower although we had already FOMC minutes that gave some hawkish remarks with FEDs playing the balancing act game. We still have labor data tomorrow that could be optimistic as we had good rebounds from Durable Goods and Industrial Production. We also have important inflation data next week and such can dictate the sentiment and the narrative if tomorrow doesn’t provide one sided data, by being totally optimistic or pessimistic. We need to remember that rate cuts on March are priced in and there is no FOMC in February so, so far expectations are to keep rates as-is still for January and high chances to be cut on March. With such, waiting for the data is key to understand the market sentiment as we also have Dollar in a bearish move since the start of October with healthy pullbacks.

We are now on this pullback since the end of the year from the 100s and it is still not breaking its bearish market structure to continue to upside as important US data is coming in the next days if no new reactive events as we are seeing headlines again from Red Sea tensions or anything related with China-Taiwan, 102.5 is now a key area and next the 104 to see more upside move.

We are now back on track and next week we will restart with our typical weekly overviews.

All the best, trade safe and stay adaptive.