Week 50 Preview

Interest Rate Decisions and Inflation data

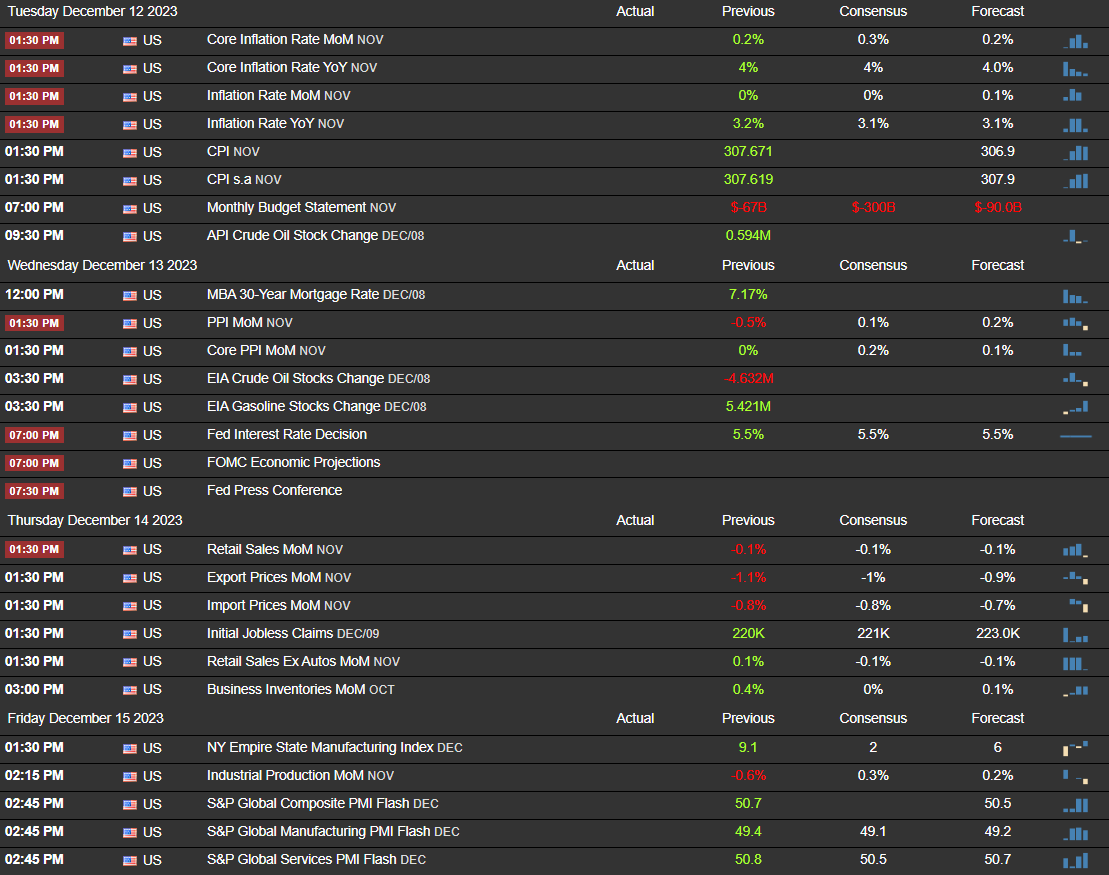

Week 50 and almost end of year with Christmas holidays incoming, this week will be very interesting in the way that we will major CB Interest Rate Decisions from FED, BoE and ECB, SEP from FED, inflation reports for US with CPI and PPI and to close of the week PMI figures.

In terms of economic events, week will start pretty quiet with lack of scheduled events on Monday where for the first half CPI will be in focus on Tuesday. CPI is expected to remain the same or even reduce in 0.1% and from what we have been seeing, some important CPI contributor factors have been declining like energy prices, retail sales, personal spending and income, for instance, are inline with high rates still in place opposing to excellent GDP projections, increase on Avg Earnings and optimal labor data according to last Friday reports. Beside these optimal readings we had and it is true that we are in months of consuming due to Thanks Giving and Christmas, our expectations is CPI to not have surprisingly data and much probably to keep the same as previous or according to forecast. Although what is important to understand in order to be able to adapt to market conditions is that we only expect decent market moves if we get surprise data in the way that lower reports feed into early rate cuts (Gold Bulls) and higher into FED to keep rates higher for longer (Gold Bears), as markets already priced in the forecast so data to come as previous will keep markets choppy and eyes will be for FOMC on Wednesday.

For us the major event for the week will not be the FOMC decision itself but the Summary of Economic Projections release where will be given to know what are the FED expectations for short and long term (same as we covered in September).

The reason is that we expect FEDs to keep rates as-is as if we remember they left the door open to one hike this year, but so far we don’t see a reason for it, so if we were to redefine the importance of economic calendar for Wednesday we would do it like the following:

The most important to be the SEP Report and the Jerome Powell speech to see if he brings more than what we will be able to read on SEP, and then the decision and short term projections, specially what and when they will be doing for 2024. For such day we recommend to wait for the dust to settle and trade after markets to digest data as usually we see continuation intraday moves.

On Thursday we will have a set of data with Retail Sales and the usual jobless claims. For Retail Sales, beside we recently had optimistic Nov. Avg. earnings and PMI reports, on services and Composite, we have seen decline in most contributors so our expectations is not to see a bounce to positive numbers, beside the season we are at. Friday to close of the week, we will have PMI figures for November, Manufacturing data and Industrial Production. Our focus, will be this last one report that is expected to rebound and the only reason we will see it to rebound (but not for so high numbers) is if the labor data reports, that we covered on our weekly recap, is confirmed with workers returning to their jobs after strikes beside the data is adjusted.

Other relevant economic events will be the Bank of England and ECB rate decision on Thursday, that for ECB already stated their position on Monetary Policy and BoE also to keep rates as is and will be interesting to see the member votes as last decision 75% voted to unchanged an 25% to hike. If you trade EU or GBP pairs during such periods you might see some volatility on such currencies if we receive surprising data as we don’t expect.

Looking at charts, On Gold and DXY, with the labor data last Friday we saw sellers pressure on Gold as such feeds into FED to keep rates higher for longer narrative. If no reactive events on Israel-Hamas conflict or other geopolitical tensions that makes markets to open with high volatility as we have been seeing for recent past, we expect a slow start and chances to Gold retest 1998s before continuing is bullish stance.

As we have important data through out the week, more downside move on Gold could be seen with data induced moves, in the way that 1970s or if 1930s might be seen if high CPI readings on Tuesday before the SEP report. On dollar will be similar in the way that to see further upside on dollar, technically we need to break 104.2s previous highs and 104.5s to head into 105s and such can happen also with the same type of data reports, else we will keep with our main bias with Bullish on Gold and Bearish on Dollar if data want change our bias as we will need to be adapting according to the reports.

To conclude it is important to back test previous events as such creates a lot of expectations on the markets due to volume and volatility that can have but we need to remember that we are in December, EoY almost on Holidays and usually we don’t have the best trading conditions. So be vigilant and stay adaptive.