Week 49 Recap

Gold to new ATHs and Yen still alive

In a week where labor market was in focus and we got some surprises, Gold gave us another new ATH at 2146.79 and Yen gave signs of life with Ueda comments on tools to tight financial conditions.

As we covered on our Week Update from 5th Dec. with markets open, Gold gave us a strong push to upside and in short minutes doing a almost 700pips move to print a new ATH with algos adjusting and creating new price points of interest and new headlines on tensions within the Red Sea bubbling up.

After such print, started a pullback until Tuesday where printed a new low of the week at 2010, which was a price point we were expecting to happen according to our weekly preview, with a potential pullback from the 2075s (the ATH of last week, without expecting such upside move to start out the week of course). Within these two days, sellers were completely in control and not even the very poor Factory Orders on Monday was able to change the sentiment and the pullback was really to occur. On Tuesday with optimistic PMI services, Gold printed a new low of the week at 2010 and reversed to form a range that lasted until the NFP day.

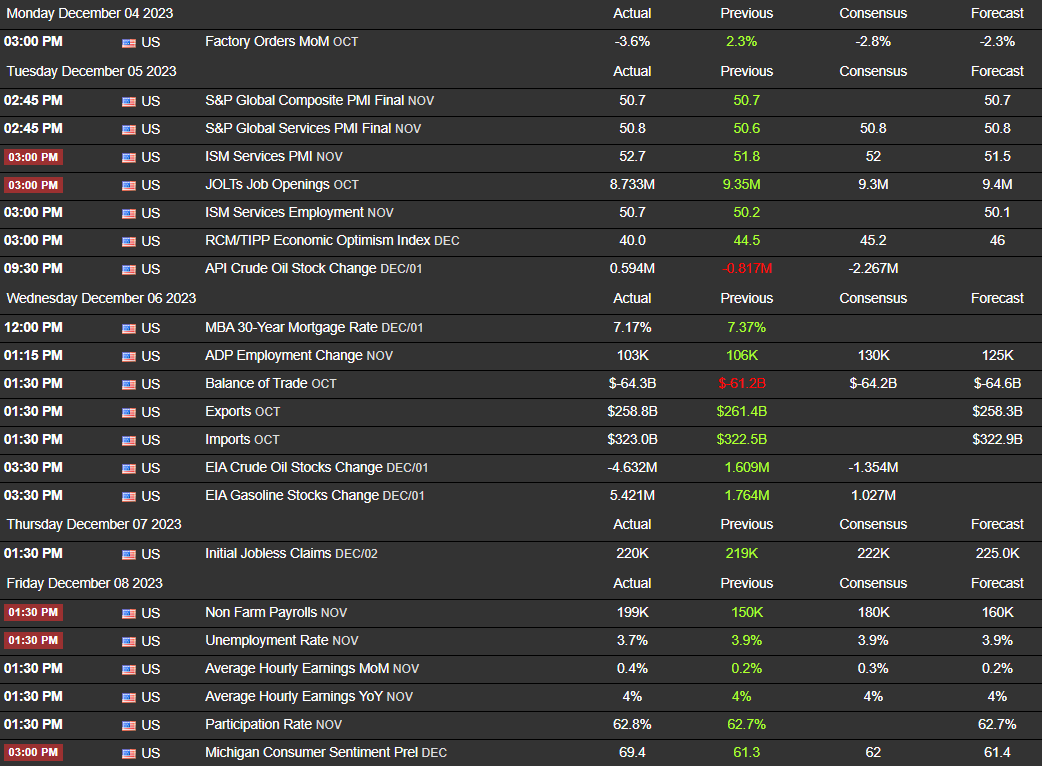

With JOLTS and ADP labor reports through the week we saw expected declines and increase on Jobless Claims of Thursday, for the reasons stated on our weekly preview, although we had some expectations if the temporary employment opportunities to cover the needs of holidays season of Thanks Giving and Christmas could create some balance on the reports, but the surprise was to come on Friday with NFP and UER.

On the week preview we stated that a slight increase on NFP would be something we were considering, but a decrease in UER was completely out of our expectations to be at 3.7% from the 3.9%.

To understand such numbers we went into the report of BLS and notice a sentence that in some way could explain such optimistic report:

Job gains occurred in health care and government. Employment also increased in manufacturing, reflecting the return of workers from a strike. Employment in retail trade declined.

Source BLS

A quick search shows that US workers from auto, healthcare and actors were on strike in September and October and such could explain the variation of the numbers from November to December reports. It is a fact that labor force is cooling due to policy lag effects and tighten financial conditions as we have been noticing it on manufacturing, industrial production and durable goods declines and so such optimistic data reported and digested by the markets with Gold breaking below the 2000s mark and Dollar retesting highs of 104.2s, much probably is not reflecting the actual scenario due to the following:

“If the striking workers earned pay for any part of the reference period, even one hour, they are counted as employed. Striking workers are reflected as a subtraction from the employment level in the first monthly estimate when they are not working in the reference pay period. They are added back only when they return to work.”

Cody Parkinson, an economist at the BLS

No matter what, our job is not to predict or verify if data is true or not but understand it and adapt to market conditions. Such optimistic report cools down the narrative of early rate cuts and that was seen already on the CME probabilities that March was suffered again a reduced probabilities of ease.

Looking at the charts, we saw a sharp decline on Gold from the 2028s to 1994s, more than 340 pips move through out the NY session. On the other hand Dollar during the week was in a bullish momentum retesting highs at 104.2s and on the NFP failed to break higher.

During the week, Dollar was able to break that visual bearish channel and as we stated, to see further upside on Dollar we need not to break the channel but the 104.2 and 104.5 to see more bullish momentum. That did not happen and beside closing the week higher than the opening price, markets didn’t gave much more even with the optimistic US labor data.

Well if we thought that labor data could only be in focus this week, on Thursday another actor came in with Yen strength, due to BoJ Ueda commenting on tools and ways on how to shift their ultra loose monetary policy into a more tightening cycle, but clearly stating that won’t hike rates yet. Markets reacted giving Yen strength and USDJPY saw a downside move of about 550pips during Asian and London session.

Of course such affected all Yen pairs across the board, but on the grand scheme of things such strong intraday move, is reflected as a minor push to upside looking at the macro perspective, although is interesting to see and this give us signs on how markets are very sensible for such policy unwind for the long years that we have been assisting to the ultra loose monetary policy.

With the week gone, now time to prepare for the next one which will be very hot with inflation reports, interest rate decisions and the most important the projections from the FED.

Stay sharp and have a great weekend.