Week 49 Preview

Labor Market in focus

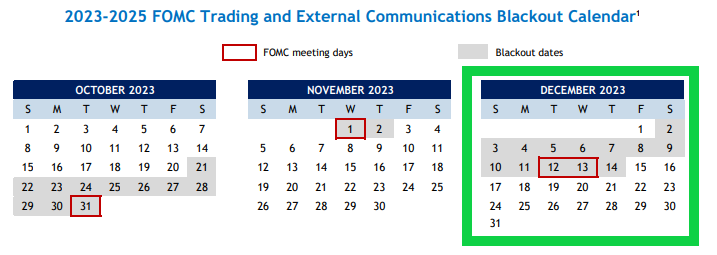

With Gold on historical highs to start out this new month and week, labor market will be in major focus. FEDs are in blackout period as next week we will have the FOMC decision, PMI and Factory Orders reports will be the first ones to lookout for.

For such new week, we will keep our stance of poor US economic data to keep Gold pushing to upside and Dollar weakness beside the the price points where gold is at the moment. So as we can see on the US economic calendar above, we will start with Factory Orders on Monday with a strong negative forecast to -2.6% due to the fact that we have seen a cooling effect on the Durable Goods, Manufacturing and Industrial production so, in order for us to see market impact we need to have values below forecast, as we do not expect to be above previous for the reasons stated. Then we will have PMI and the first employment data report of the week. PMI services are still in healthy territories and are expected to increase although we need to bear in mind the cooling effect on labor, sales and spending, we have positive consumer confidence, as the report at end of week "Mich. Consumer Sentiment” is also expected to increase. So for such reports we need to be cautious because at the same time we JOLTS that is expected to decrease and mixed data today would lead to Gold to range as we saw last week.

On Wednesday, another labor report with ADP that is expected to rise for Nov. period. It won’t be something that we shouldn’t consider in the way that big retailers often create more jobs to answer to the season demands although data we receive is seasonally adjusted.

Amazon plans to hire 250,000 US workers for holiday season

Source - Reuters

For Thursday, our weekly Jobless claims with same expectations to rise and on Friday the most expected report of the week with UER and NFP.

The last NFP and UER report we had cooling data as we saw UER to increase and NFP to reduce, this time the expectations are NFP to increase and UER to keep as-is. For our perspective would be good to have one sided data here for better market moves with either bad or good data, although we are seeing cooling signs on labor and manufacturing, a slight increase could indeed occur on NFP after such a sharper decrease on October, where it came from 297k to 150k as we can see below. On the other hand a 3.9% on UER according to expectations is still in line with FED, beside their last projections were to unemployment be at 3.8% EoY, but this report is for November so only in January will see the result for 2023.

At the same time of Labor data, we also have Avg earnings that we shouldn’t disregard as that contributes for income and spending so consequently for inflation. If we see neutral labor and robust report this could hold more weight as we have seen such happening in the past. Last but not least, we will have Preliminary Mich Consumer Sentiment for Dec that we already stated they are expected to increase due to the season, similar to the last CB Consumer Confidence.

During this week and until 14th Dec, where we will have FOMC decision report at 13th, FEDs are in blackout period as we referred on our previous week preview and so nothing from them for us to be vigilant on.

Before looking into the charts it is important to realize that such week will be the last before FOMC and for us the important thing to lookout for will be the Summary of Economic Projections and we get to know what will be the FED expectations in short and long term. It would be very interesting and healthy for us to see a potential pullback on Gold to collect more buy orders for a better price demand because, and giving a glimpse of what is to come, Friday (8th) Labor data, Tuesday 12th CPI and Wednesday 13th PPI and FOMC, Gold is at ATHs and for what is to come it makes sense for us to see such pullback.

As we can see on Gold, since the start of Israel-Hamas Conflict Gold came from 1810 to 2010 and only after a period of accumulation did an healthy pullback from the 2010s to 1930s to a better price demand collecting more buy orders to create new ATHs and since then just minor pullbacks respecting such bullish market structure capable to be seen with such visual representation of trend lines. On the other hand, DXY after breaking that accumulation zone in October between 105s and 107s, sellers jump in and were taking profits along the path with buyers providing such exit relief but kept always price under control creating a very healthy and organic bearish market structure.

With such, I would like to see Gold to create such pullback to 2050s or even to 2010s important supply zones for what is to come to potentially close of the year in highs together with equities. Although we need to be prepared and be able to adapt to market conditions as Early Rate Cuts by FEDs is main information advantage with CB Monetary Policy is what is still driving the markets and if no other third party factors contribute to market moves, US economic data will be key for such to happen.

Be vigilant for any upcoming headlines on potential Geopolitical tension, stay safe and trade smart.