Week 2 - Overview

Important US Inflation data incoming

With holidays season and events already gone, we will enter on the first full week of markets open of 2024. All eyes on important US inflation data on the last half of the week could potential give a quiet start as no relevant expected data reports are occurring during the first half.

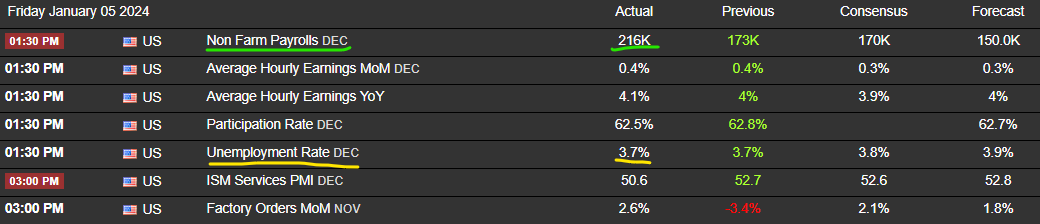

As we already summarized what happened during our holidays period and brief year preview on Gold, before we jump in to the week overview, let’s look what happen last Friday with US jobs data.

According to our recap we gave expectations that good US jobs data might be released due to other economic indicators that could suggest healthy labor data and in fact NFP came against expectations at 216k and UER same as previous 3.7%.

“We still have labor data tomorrow that could be optimistic as we had good rebounds from Durable Goods and Industrial Production.”

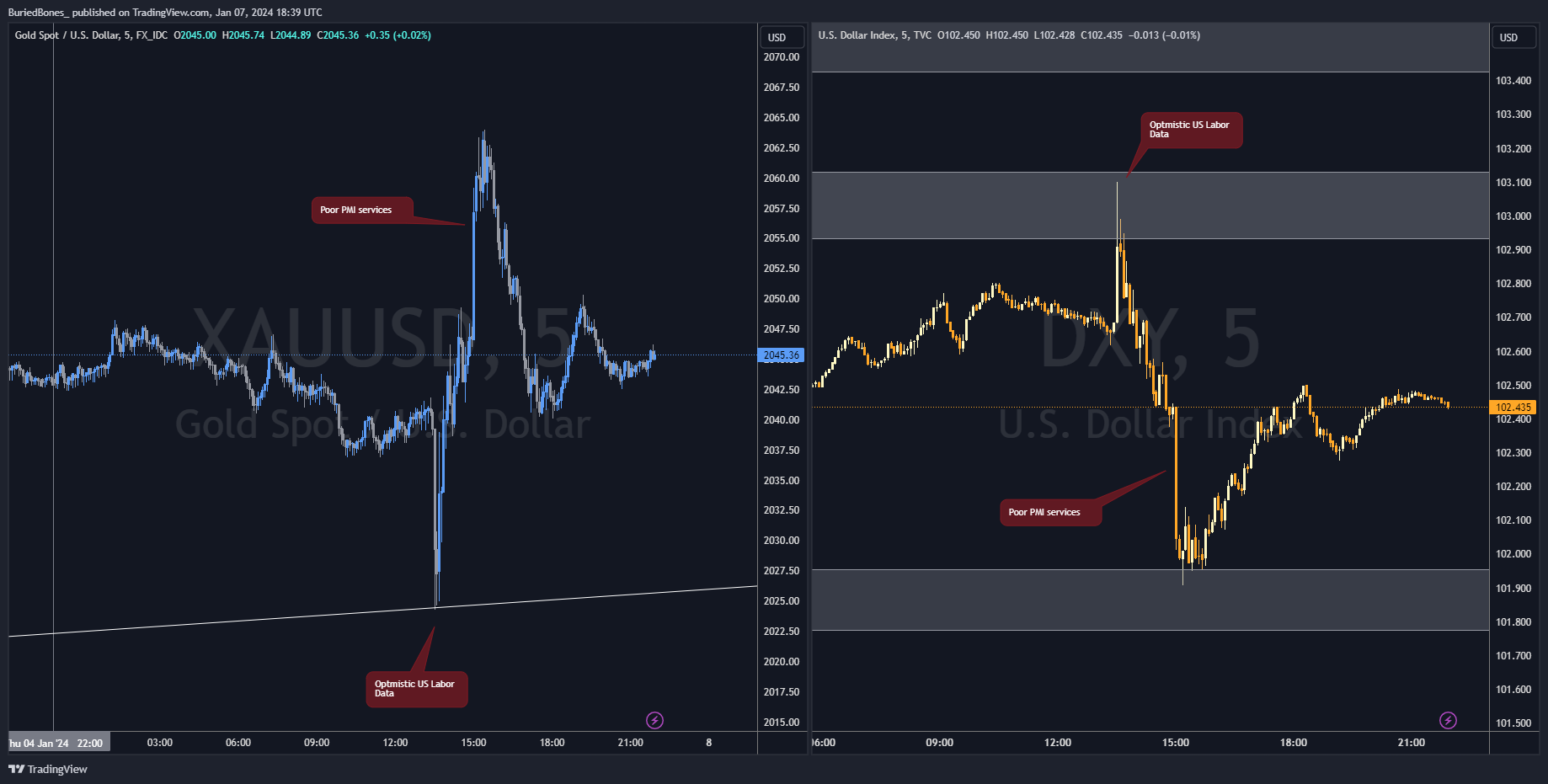

The biggest contributor for employment was the government followed by hospitality and leisure and the interesting fact about such report is that it was the last report of 2023 showing us that during the last year we had about 2.7M job gains which gives an average of 225k per month and it was the smallest gains since 2019 excluding of course the 2020 pandemic year. On the UER we had 0.2% higher than Dec. 2022 but below the FED projections of 3.8% according to the last SEP report. Translating such into the markets, such data would suggest a bearish move on Gold and bullish on Dollar as it goes against the “Rate cut Sooner” narrative but in favor of “higher for longer”. But what we saw was just a pullback on Gold from 2039s to 2024s on the news event and a complete rejection that push almost 400pips up into NYSE with poor PMI services and that feeding into “rate cut sooner” narrative.

Of course that such move was against our expectations (hence why we got a break even sell on Gold) and that show us that narrative is holding more weight and such labor data was not enough for economists and investors to switch their sentiment yet due to optimistic data and as daily closed mainly in the same price area, so we need to wait if inflation reports would change anything.

This bring us to what will happen this week as the second half is what will have more market impact if no reactive events would come.

As we can see the first half will be pretty quiet as no major economic reports and that could translate for the markets to be ranging, in a secondary stage, as all eyes will be focused on Thursday 11th for Inflation reports.

According to the economic calendar we can see mixed expectations as IR to increase but decreased for Core IR. Our view and according to previous economic indicators is that we can also see inflation to increase as we had positive rebounds on Retail Sales, Personal Income & Spending, Consumer Confidence, etc all of them contributors to inflation increase, although this goes against the major contributor factor which is energy, as such prices still saw a decline during December, so it will be interesting to see how it will be balanced. Nevertheless, our job is not to predict but to understand the market impact of such reports and best is if we could have one sided data scenario that an overall decrease of inflation would feed into the current narrative with Gold pushing higher and Dollar bearish, but with an increase we need to be cautious here as minor increase above forecast could give Gold bears and Dollar bulls much probable only for short term as we saw last Friday with labor data, but higher surprised data (which we personally don’t see it happen, unless data being cooked by BLS… something we already saw happen before, exactly one year ago) could give the same market behavior but for longer and in that case we need to assess if there will be a sentiment shift by analyzing specific price points of interest and waiting for market structure to form on intraday time frames. The other scenario we usually don’t want is mixed data as such could lead to indecision providing unfavorable market conditions.

Until there we have low expectations on market movement if, of course, no major reactive events on Red Sea escalation tensions, as we have still well priced in two wars running, or other geopolitical tensions that could arise. For such, be vigilant because we are still very early on new year and month with potential price setups still forming.

As we can see, Gold is still technically bullish with lower highs being printed since the start of Israel-Hamas conflict and for such to turn bearish we need to see breaks of such market structure fundamentally supported by any catalyst that could shift the current sentiment and narrative in play. On the DXY side, as we have been bearish, with Friday data we saw similar whipsaw as Gold and still closing within the 102.5 important price area showing signs the buyers are not yet in control as they failed to hold price above it.

Stay vigilant and adaptive and be safe.