Week 38 - Interest Rate Decision Week

US Federal Reserve, BoE and BoJ rate decision and Jerome Powell speech

After the US CPI readings and ECB rate decision for 25bps, now is time for FEDs, BoE and BoJ to make their decisions.

This new upcoming week that will be marked by rate decisions from major central banks and the finish of blackout period from FEDs. Monday and Tuesday might be quiet due to lack of economic events that could hold weight on the markets, unless any reactive headline that came out suddenly and we need to adapt accordingly.

Beside on Tuesday we will have reports of inflation rate on EA, we have not much expectations on market impact since the monetary policy for ECB is pretty much defined and decided for the next quarter. There will be a pause on hikes at least until end of 2023 and in 2024 they will assess if it is needed, of course, according to data reports. So, such type of economic reports might not hold much weight unless any changes or any data brings back pressure that forces ECB to review. Remember that for the last two years markets world wide have been driven by Central Banks Monetary Policy decisions, with tighten conditions (except Japan). On 2022 pretty much we had Gold Sells and Dollar buys since the start of the biggest rate hike cycle in US history, until October where we saw a pivot narrative to come in place that switched the sentiment. We as retail traders must follow same approach as FEDs “take action according to data reports” day by day, report by report.

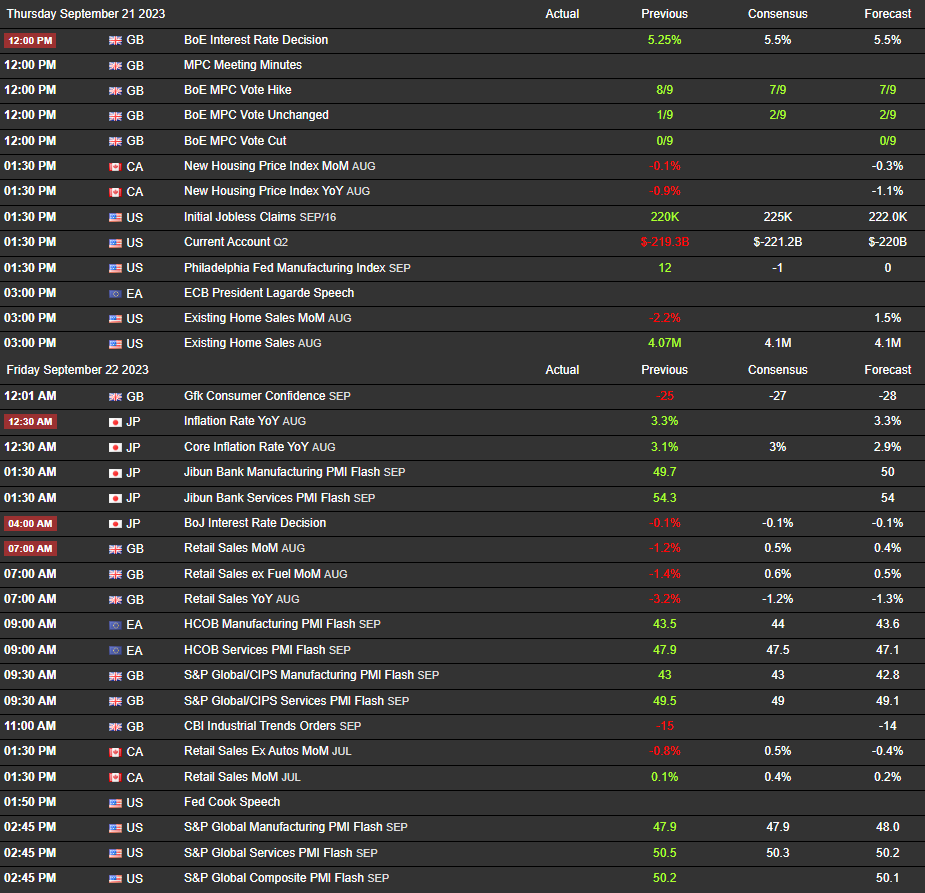

On Wednesday we will start with GBP data on pre-London in regards to Inflation report before BoE decision. later in the day I would love to have some volume and volatility on Gold during FOMC and press conference, but I think we should decrease the expectations not only because the no hike is completely priced in and JP speech might not bring anything new to the table. A no rate hike is almost unanimous within investors and economists where CME group sets to 98% of such probabilities to remain unchanged and to note that since the beginning of August that this probabilities are above 80%.

Unless there is any surprise, like a hike or JP to bring any dates when to pivot or something, judging for the last FOMCs and JP interventions with his careful approach to not shake the markets and with easy Q&A after I don’t expect much volume nor volatility (similar to last CPI report, not much compared to what we had in 2022), but I would love to be wrong :)

On Thursday, it’s time for BoE to decision. An expected increase is on the table and I believe that they will do even if the inflation report can be below previous. The reason is that inflation is still to high and according to data reports, UK is not in bad condition as EA for instance and economy can handle another hike, but we will see. On Friday, to close of the week, we will have during Asian session Japan data with inflation report and BoJ decision. Here expectations to keep everything as-is are high beside that Ueda comments last week after market close. But remember that Japanese sometimes can “drop some gems” out of nowhere in order to strength JPY. Since we have a important reports on GBP and JPY for the mid-end week we could expect some volume and volatility in such pair.

Trade Safe and Trade Smart.